China Zhongwang 2015 Net Profit Rises 13.2% to RMB2.8 Billion

Gross Profit Margin Increases Year-on-Year to 32.9%

* * *

Proposed A-Share Spin-off of Industrial Aluminium Extrusion Business

Will Substantially Increase Corporate Value

(Hong Kong, 24 March 2016) – China Zhongwang Holdings Limited ("China Zhongwang" or the "Company", together with its subsidiaries the "Group", stock code: 01333), the world"s leading aluminium fabricated product developer and manufacturer, announced its audited annual results for the year ended 31 December 2015 (the “Year under Review”).

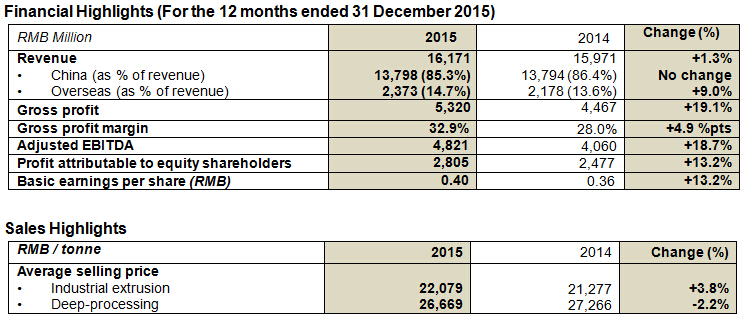

During the Year under Review, the economic growth of China and the global markets continued to slow down. The Group gradually adjusted its production capacity and optimized the product mix by further increasing investments in technology as well as research and development (“R&D”), thereby improving its profitability and achieved total revenue of approximately RMB16.17 billion, representing a slight increase when compared with that of 2014. As the revenue contribution from high-end products increased, the overall gross margin increased by 4.9 percentage points to 32.9% year-on-year. Profit attributable to equity shareholders increased by approximately 13.2% year-on-year to approximately RMB2.80 billion, and basic earnings per share rose to RMB0.40. To reward shareholders for their support, the Board has recommended a final dividend of HKD0.06 (approximately RMB0.05) per share for the financial year ended 31 December 2015. Together with the interim dividend, the dividend per share for the year totalled HKD0.17 (approximately RMB0.14), which is equivalent to a dividend payout ratio of approximately 35.4% on a full-year basis.

Mr. Lu Changqing, President and Executive Director of China Zhongwang, said, “China’s economy is entering a new normal phase of steady growth while economic growth has shifted from the previous mode of quantity first to the new mode of focusing on both quantity and quality, bringing unprecedented development opportunities for the aluminium processing industry. We adhered to the strategy of “primary focus on China, complemented by overseas markets”, continued to dedicate efforts on the China market, and promoted the application of high-end aluminium processed products in the sectors of transportation, machinery and equipment, and electrical engineering. During the Year under Review, we continued to leverage the internal synergies of our three core businesses, namely industrial aluminium extrusion, deep processing and aluminium flat rolling businesses. The Group actively enhanced its R&D as well as innovation, optimized product mix, enhanced production technologies, strengthened internal management, and further consolidated core competitive strengths and profitability, to achieve the encouraging results for 2015.”

Proposed Spin-off of Aluminium Extrusion Business to Unlock the Corporate Value

The Group entered into an asset purchase agreement with CRED Holding Co. Limited (“CRED Holding”, SSE stock code: 600890) which is listed on the Shanghai A-share market. CRED Holding agreed to purchase the total equity interests in Liaoning Zhongwang Group Co., Ltd. (“Liaoning Zhongwang”) that focuses on industrial aluminium extrusion business. The initial appraisal value of Liaoning Zhongwang is approximately RMB41.7 billion. After deducting the proposed post-Reference Date dividend of approximately RMB13.5 billion to a subsidiary of the Group, the total consideration of the transaction will be RMB28.2 billion. It will be settled by issuance of approximately 3.93 billion Consideration Shares by CRED Holding to China Zhongwang at RMB7.12 per share. Meanwhile, CRED Holdings plans to allot and issue by way of non-public offer to raise proceeds of no more than RMB 5 billion for the development of Liaoning Zhongwang Group. After the completion of the transaction and the share placement, China Zhongwang will hold about 75% of the enlarged share capital of CRED Holdings. Through injecting its extrusion business into CRED Holding, China Zhongwang will achieve a spin-off on the A-share market. Upon completion, the A-share listed entity will provide the Company a new financing platform, while the Hong Kong listed entity will have a more distinctive business focus and competitive strengths. These will benefit the Group’s long-term development and create value for its shareholders.

Extrusion Business – Optimized Production Capacity and Product Mix to Raise Gross Profit Margin

During the Year under Review, sales volume of the Group’s aluminium extrusion business was approximately 660,000 tonnes, with sales revenue of approximately RMB14.14 billion, basically in line with that of 2014. As the core production facilities were operating at full capacity, the Group replaced or underwent technical upgrade for some older equipment in order to improve production efficiency. It also helped customers to develop more high-end products to increase the contribution of high value-added products. This has strengthened its overall profitability. Coupled with a decrease in aluminium ingot prices, the gross margin of the Group’s aluminium extrusion business further increased from 25.4% for 2014 to 30.0% for the Year under Review. The Group has ordered two ultra-large 225MN extrusion presses, which are the largest and most advanced in the world. One of the presses has been delivered at Yingkou plant for installation. The operation of the 225MN extrusion presses will reinforce the Group’s leading edge in the production of high precision, complex large-section industrial aluminium extrusion products.

Deep Processing Business – Diversified Products with Breakthrough in Transportation Applications

During the Year under Review, sales volume of the Group’s deep processing business increased by 15.5% to approximately 73,000 tonnes. Sales revenue increased by 13.0% to approximately RMB1.95 billion, and gross margin increased from 31.8% for 2014 to 32.5% for the Year under Review. The range of the Group’s deep-processed products is becoming more diversified, among which the contribution of aluminium parts and components for new energy vehicles and buses is gradually increasing. The Group possesses comprehensive capabilities from independent design to manufacturing and processing, and made significant breakthroughs in various designs including aluminium-intensive new energy battery electric vehicles (BEVs) and the integrated design of aluminium battery frames. The Group has commenced technological cooperation with several well-known domestic bus and vehicle manufacturers to jointly develop aluminium-intensive new energy buses and BEVs. The Group has reserved sufficient resources for the long-term development of the deep processing business, in order to make necessary investment and capacity expansion in a timely manner.

Achieved Breakthrough Progress in Several Key Projects under Construction

During the Year under Review, the first production line of phase one of the high value-added aluminium flat rolled product project in Tianjin has entered an important stage prior to its commercial operation. Core and ancillary facilities have completed trial runs. The production line is currently undergoing final testing on products of different alloy combinations, and conducting trial production on sample orders for clients. In the second half of 2015, the smelting and casting mill successfully produced aluminium alloy ingots at its first attempt. The first batch of aluminium alloy plates and aluminium alloy coils were successfully produced by the hot rolling line and the cold rolling line respectively, marking a significant progress of the project.

The Group’s high-precision aluminium and special aluminium alloy project located in Yingkou, Liaoning Province, with a designed annual production capacity of 400,000 tonnes, was completed and commenced production during the Year under Review. Approximately 290,000 tonnes of high-quality aluminium alloy raw material were produced for the Group’s internal production during the Year under Review. One of the two ultra-large 225MN extrusion presses is under installation and production is expect to commence in 2017. The other press will be delivered for installation during 2016.

In addition, Liaoning Zhongwang Special Vehicle Manufacturing Company Limited (the “Special Vehicle Plant”), a wholly owned subsidiary of the Group, has obtained various licenses for the production and sale of a number of aluminium-intensive commercial vehicles during the Year under Review. The two production lines currently under construction will manufacture aluminium-intensive semi-trailers and oil tank trucks respectively. The sales team is in close contact with potential customers in a bid to achieve volume sales within this year.

R&D and Innovation – Optimized Product Mix and Strengthened Overall Competitiveness

During the Year under Review, the overall R&D expenditures of the Group amounted to approximately RMB510 million, accounting for approximately 3.1% of total revenue. Being a High and New Technology Enterprise, the Group continued to enjoy the preferential rate of 15% for Corporate Income Tax. Thanks to the efforts of the R&D team, the Group developed over 100 new products, attained 13 technology and new product awards at national, provincial and municipal levels and filed 93 patent applications in 2015. The outstanding R&D capability is the cornerstone in strengthening the Group’s comprehensive competitiveness.

“The Chinese government has promulgated a number of macro-economic policies in support the high-end application of aluminium in the transportation, machinery and equipment, and electrical engineering sectors.” Mr. Lu concluded, “Looking into 2016, we will push forward the commercial production of the first production line of the aluminium flat rolled product project in Tianjin as well as the Special Vehicle Plant. At the same time, we will continue to optimize the equipment and production capacity of the industrial aluminium extrusion business and committed to R&D investments to increase the proportion of high value-added products. Embracing a market with immense potentials, the Group will leverage its full-fledged business model, including three major industrial aluminium extrusion, deep processing and aluminium flat rolling businesses as well as our high-precision aluminium casting capacity. We aim to spearhead the industry development and capture the opportunities arising from the industrial upgrade in China, ultimately providing sustainable returns to shareholders in the long run.”